This article is provided FREE for Google searchers. In order to access all content on Marcellus Drilling News, please visit our Subscribe page.

A 30-inch segment of Enbridge’s Texas Eastern Transmission Company (Tetco) interstate natural gas pipeline exploded in January, sending two people to the hospital and destroying two nearby homes when fires from the blast spread (see Texas Eastern Pipeline Explodes in Noble County, OH – Injuries). The pipeline is now, after 10 weeks, fully back online and flowing at 100% capacity. We have an update on how the outage affected flows in the region, and the likely cause for the explosion.

Some 2.31 billion cubic feet per day (Bcf/d) of Utica Shale natural gas had been flowing through the Berne Compressor Station in Noble County, OH. Some (most?) of that gas goes to the Gulf Coast via the Tetco. Following the Tetco explosion, that 2.31 Bcf/d coming from Berne dropped to 0 Bcf/d. Yet eight days after the explosion partial service was restored (see Enbridge Trying to Restore 1 Bcf/d on Exploded Tetco in Ohio). How can that be?

What we didn’t understand when first reporting the story is that the Tetco pipeline in the Berne area is not one pipeline, but three pipelines–all laid near each other along the same right-of-way. It was, according NGI, Line 10 that experienced the explosion. Lines 15 and 25 were shut down along with Line 10 “just in case” there was damage to them. Enbridge checked and double-checked and restored service to Line 25 eight days after the initial explosion. Enbridge later restored service to Line 15. And now, according to RBN Energy, Line 10 is back too.

RBN has a great post that delves into the Tetco outage in Ohio, how it affected flows in the region, and how it affected drillers (in the Utica) and end-users (in the Gulf).

Ten weeks after an explosion crippled a key natural gas takeaway route out of the Marcellus/Utica, the capacity finally has been fully restored. Texas Eastern Transmission two days ago said it’s lifting all restrictions on the affected section of pipe. The outage began on January 21 and partial service resumed eight days later, but TETCO’s Northeast production receipts during the event averaged about 700 MMcf/d lower than usual and the line’s flows to the Gulf Coast were cut by 30-40%. That, along with two severe polar-vortex periods in January that overlapped with the outage, caused a reshuffling of flows across other pipelines in the region. Today, we wrap up this series with a look at the implications of the outage on the Northeast gas market and what to expect now that it’s ended.

Last fall, in our Dog Days Are Over? series, we previewed a potential turning point in the Appalachian gas market, from the supply region being severely constrained for years to being well-connected with the ability to better balance its excess supply with outflows. As we’ve discussed extensively in the RBN blogosphere, takeaway constraints in the Marcellus/Utica producing region have for years been depressing local prices at regional trading hubs like Dominion South and Tennessee Zone 4/Marcellus, trading well below the national benchmark Henry Hub, even during the winter months when Northeast demand peaks. But a number of pipeline expansions came online in the summer and early fall of 2018, and pipeline utilization for flows out of the region seemed to suggest that takeaway capacity had finally caught up, with room to spare, at least for the time being. (We’ll come back to the specifics of that “spare capacity” in a future blog.)

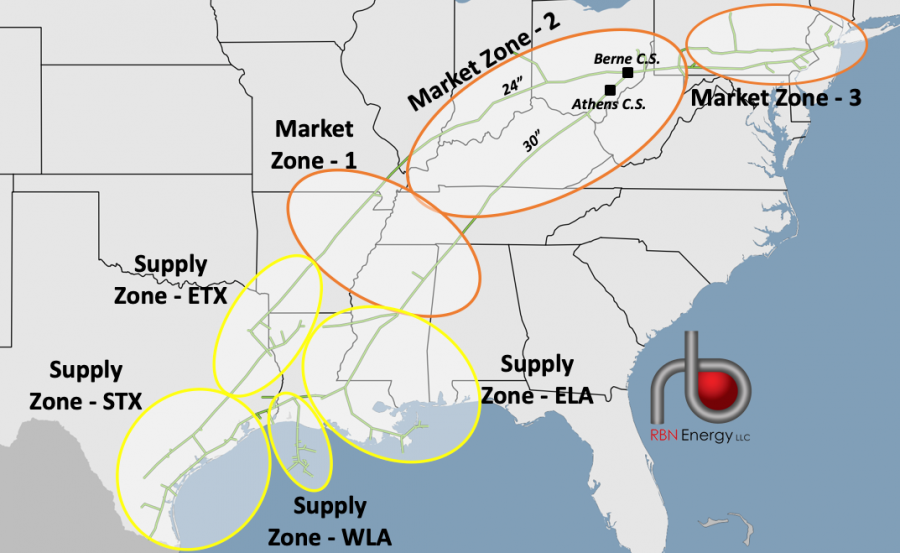

Then, on January 21 (2019), TETCO — an important takeaway route from the Marcellus/Utica — experienced an explosion and subsequent outage, reducing southbound capacity on its “30-inch” line and putting the new “unconstrained” reality to the test. (Note that while the leg is called the “30-inch” line by legacy, the pipe now includes multiple lines in the ground along that path.) The location of the outage in Noble County, OH, shut down flows through the Berne compressor station, severing the connectivity between Northeast supply and downstream Gulf Coast demand, and bifurcating the pipe into two, with its northern zone moving Marcellus/Utica supply to the East Coast market areas (Market Zone 3; orange oval to far right in Figure 1) and, the more southern portions of the system (everything south of the Berne compressor station) left to source supply from Louisiana and Texas — like in the days before the Marcellus/Utica’s growth and TETCO’s reversal. As we noted above, the full outage lasted only a few days, with partial service resuming by January 29, but until yesterday the line’s capacity remained reduced at 1.6 Bcf/d, or 70% of its normal capacity. Keep in mind, the outage overlapped in its early days with two extreme weather events — the coldest days of this winter, in fact — in mid-January and again in late-January/early-February. These events factored heavily into flows and price response in that they helped absorb any excess Marcellus/Utica supply and, beyond that, pulled significant volumes north from the Gulf Coast, not just on TETCO, but on other long-haul pipes.

As we noted in the previous episode, the January 21 explosion had distinctly different impacts on its downstream markets in the Gulf Coast versus the Northeast. In Part 1, we looked at the immediate effects of the outage on southbound flows and Gulf Coast markets and concluded that while TETCO’s supply receipts at Berne were curtailed, the pipeline’s interconnectedness made it possible for its Gulf-area gas supply receipts to ramp up and offset the loss of Marcellus/Utica supplies. As a result, its Gulf-area deliveries were able to remain relatively steady. What’s more, TETCO, which had been flowing about 2 Bcf/d south from Berne into Louisiana in the year prior to the outage, began flowing northbound up to Berne to help meet demand along its market zones 1 and 2 south of Berne (orange ovals toward the middle of Figure 1).

The bottom line is that flows south of Berne were able to reshuffle to minimize volatility. Next, we turn our attention to how it has affected the Northeast producing region.

Figure 1. TETCO Pipeline Zone Map. Source: RBN (Click to Enlarge)

We should start by noting that an outage like this in past years likely would have severely constrained Northeast production and sent already-discounted Marcellus/Utica supply-area prices reeling to even deeper discounts relative to their downstream markets, including Henry Hub — yes, even in the winter. However, two key factors disrupted that dynamic this time around. We mentioned one of those above — the extreme cold weather events, which helped absorb more Marcellus/Utica supply locally, and also pulled significant volumes north from the Gulf Coast, not just on TETCO, but on other long-haul pipes too.

From a more big-picture standpoint, the other major factor is one we also touched on in the previous episode, namely the emergence of “super header” pipelines and the overall excess takeaway capacity in the Northeast. The role of TETCO (and other legacy Gulf-to-Northeast pipes) has drastically changed in recent years, from being a linear, long-haul system to being a bidirectional “super header” with numerous entry and exit points along the way. As we discussed in Part 1, TETCO was one of the first legacy long-haul pipes to enable bidirectional flows and connect Marcellus/Utica gas supplies to the Gulf Coast through a series of reversals and expansions. And, overall in the Northeast, more than 5 Bcf/d of takeaway expansions have come online in just the past two years. As that’s happened, basis in the supply region (i.e. supply-area prices relative to Henry Hub) has recovered from trading as much as $2.00/MMBtu below Henry Hub a couple of years ago to hovering around $0.50/MMBtu below Henry in the past year, which is close to the variable transportation cost ($0.15-$0.40/MMBtu for TETCO M2). That half-a-buck basis held even during the outage, demonstrating that supply has some running room to leave the region currently. Besides adding takeaway capacity, these expansions and new pipeline additions have improved the overall connectivity in the region, providing producers with options to move their gas. The spare takeaway capacity and added connectivity, along with the robust demand this winter, gave shippers the flexibility to redirect gas flows around the outage, thereby minimizing the impacts to the grid, and preventing reliability issues and significant price blowouts.

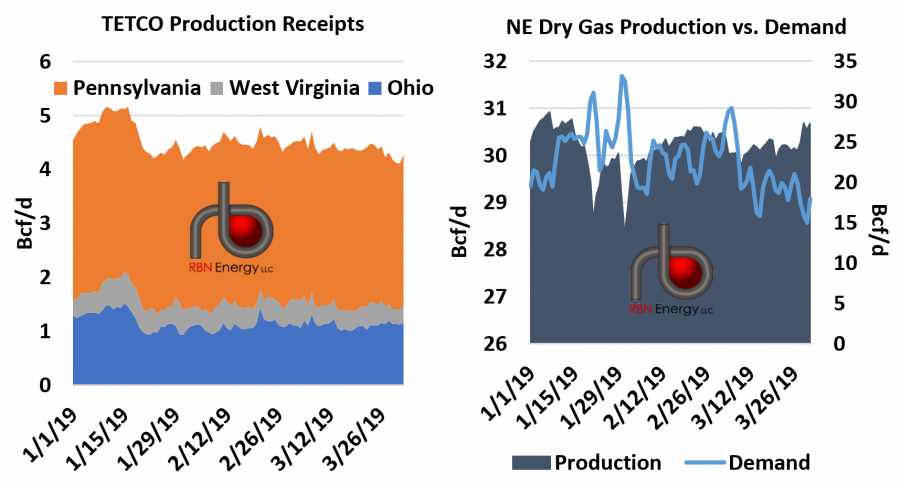

That said, the Northeast wasn’t completely unscathed by the outage. Overall, regional production receipts fell, just not as much as they would have a few years ago when producers had fewer takeaway options — or if the TETCO outage had occurred in a low-demand month. On the first day of the outage, production receipts on TETCO (total of the three layers in the left graph in Figure 2), dropped by 600 MMcf/d from the month’s high (production was already down from cold-weather related freeze-offs in the days before the outage) — from upwards of 5 Bcf/d to ~4.4 Bcf/d. As partial service on TETCO was restored by January 29, receipts rebounded somewhat, but they mostly have remained below 4.5 Bcf/d.

Unsurprisingly, Ohio production receipts (blue area, left graph) took the largest hit and have been the slowest to rebound. Prior to the outage, production receipts in Ohio averaged about 1.35 Bcf/d. Since partial service was restored, they have been between 900 MMcf/d and 1.2 Bcf/d, spiking up above that on a handful of days, but always accompanied by a spike down in production receipts elsewhere, largely in West Virginia (gray area, left graph in Figure 2), and particularly on warmer weather days. In other words, supply receipts from other areas are competing for the more limited exit capacity on TETCO’s line. During winter, this was less of a concern, because eastbound flows to serve heating demand and deliveries to other area pipes were able to absorb the additional supply.

Figure 2. TETCO and Appalachia Production Receipts. Source: Genscape (Click to Enlarge)

By comparison, total Northeast gas production (navy-blue area and left axis in the right graph in Figure 2), which was already down prior to the outage, initially also fell nearly as much — by about 850 MMcf/d on January 21 — to just under 29 Bcf/d (the first deep valley in the navy-blue area). That dip coincided with a demand spike (aqua-blue line, right axis), which indicates that extremely cold weather likely contributed to freeze-off-related production losses in the basin, while also requiring that more supply stayed in the region to help meet heating demand. However, as the cold weather abated, overall regional production bounced back by more than 1 Bcf/d over the three days that followed, even as TETCO receipts remained lower — suggesting that other pipelines were able to pick up the slack. Another polar vortex event came at the end of January, and again, Northeast production fell off abruptly (second deep valley in navy-blue area), only to recover to the 30-Bcf/d level in the first week of February.

In other words, the cold-weather events were likely a bigger factor in Northeast production declines during that time than the pipeline outage — a testament to the numerous pipeline reversal and expansion projects in recent years that have cleared constraints and opened up producers’ takeaway options, save for a few isolated areas.

The price response in the Northeast also was more or less in line with other extreme cold weather events, given that the TETCO outage didn’t have much of an effect on in-region deliveries. Nor did the pipeline outage cause downward pressure on the region’s supply-centric price hubs (i.e., Dominion South Point), considering that the spike in heating demand helped absorb the gas that would’ve otherwise flowed south to the Gulf Coast. We should note that the TETCO outage and polar vortex events coincided with a couple of other events that complicated the price response: 1) TETCO experienced another outage at its Marietta Compressor (in M3 near the Philadelphia area) during the polar vortex event; and 2) the Mariner East 1 pipeline, a key outlet for NGLs out of Marcellus/Utica, was shut down on January 21.

To sum up, the fact that the TETCO outage occurred during a high-demand period limited the amount of Marcellus/Utica production that had to be curtailed, because more gas was able to flow east and serve Northeast demand. That, in turn, helped support regional prices there. With the capacity now restored, the market is saved from having to answer the question of what would happen if this dragged into a shoulder month, when Northeast demand drops and more gas needs to flow out of the region. Cash prices over the past couple of weeks — when demand already had moderated quite a bit — were relatively sanguine, indicating that the market would largely have been able to absorb it. Or, perhaps, the outage ended just in time. Regardless, with the 30-inch line’s capacity now fully back in service, we expect another regional reshuffling to occur. Recall that TETCO has some of the oldest southbound capacity — it was one of the first Northeast pipes to reverse flow direction to move gas south out of the Marcellus/Utica — and it’s at the bottom of the takeaway stack of outbound pipes, meaning that it fills first. Thus, production receipts that had shifted to other pipes during the outage are likely to shift back to TETCO’s 30-inch line, where flows should rebound to above 2 Bcf/d in very short order (up from the ~1.5-Bcf/d level we’ve seen the last couple of months). That is more or less where flows were prior to the outage and also this time last year.

Northeast gas production going into injection season is averaging close to 4 Bcf/d higher than this time last year. Undoubtedly, there will be record amounts of Marcellus/Utica supply looking to flow out of the region. Regional basis typically is weaker during the shoulder season as it is, and maintenance events or outages would put additional pressure on those prices. However, given the region’s newfound ability to shuffle flows between the pipes and the current slack in general takeaway capacity from the region, any such events likely will have much less of an impact than they would have a few years ago, and likely not be enough to widen basis out to the ultra-constrained level of years past. (1)

Coincidentally, we also noticed an article that pegs the cause of the explosion as a landslide:

Federal regulators and Enbridge Inc. officials say they believe earth movement was a factor in a January explosion on a gas pipeline in a hilly corner of Ohio.

The explosion on the Texas Eastern Transmission pipeline injured two people and damaged two homes (Energywire, Jan. 23). The 30-inch line blew up Jan. 21 near Summerfield in southeastern Ohio.

“It appears that earth movement was a factor,” a company spokesman told E&E News. Officials with the Pipeline and Hazardous Materials Safety Administration said that was consistent with their preliminary understanding.

Earth movement — such as landslides, erosion and sinkholes — can strain pipelines, leading to ruptures, spills and explosions. Pipelines in the mountainous Appalachian region have been bedeviled in the past year by landslides and other problems resulting from land movement. The landslides have often been linked to unusually heavy rains the area has experienced.

…

An Enbridge statement on the Texas Eastern Transmission explosion said the company’s operations and integrity staff was able to rule out numerous factors other than land movement. The company expects to prepare a “root cause analysis” report.

The incident data available from a database on PHMSA’s website yesterday listed the cause as unknown.

The incident data, provided by the company in February, indicated Enbridge was notified of the rupture by a member of the public. It also indicated the area of the explosion was isolated via manual valves.

The section that exploded was built in the early 1950s. An in-line inspection of the pipeline was performed in 2012, and the company said no remediation was needed.

The pipeline consists of several lines. Two, called Line 15 and Line 25, have been returned to operation. The damaged pipe, Line 10, remains down, and the company says it plans to reopen it “in the near term.”

“Safety remains our top priority,” the company’s statement said, “and everything we are doing is driven by our commitment to the community, its safety and the safety of others.” (2)

Notice that the second story above says Line 10 is still down but will reopen “in the near term,” yet RBN says full capacity has been returned. We elect to believe RBN in this case.

A 30-inch segment of Enbridge’s Texas Eastern Transmission Company (Tetco) interstate natural gas pipeline exploded in January, sending two people to the hospital and destroying two nearby homes when fires from the blast spread (see Texas Eastern Pipeline Explodes in Noble County, OH – Injuries). The pipeline is now, after 10 weeks, fully back online and flowing at 100% capacity. We have an update on how the outage affected flows in the region, and the likely cause for the explosion.

A 30-inch segment of Enbridge’s Texas Eastern Transmission Company (Tetco) interstate natural gas pipeline exploded in January, sending two people to the hospital and destroying two nearby homes when fires from the blast spread (see Texas Eastern Pipeline Explodes in Noble County, OH – Injuries). The pipeline is now, after 10 weeks, fully back online and flowing at 100% capacity. We have an update on how the outage affected flows in the region, and the likely cause for the explosion.